Why global debt keeps rising even after the crises end

Five charts to start your day

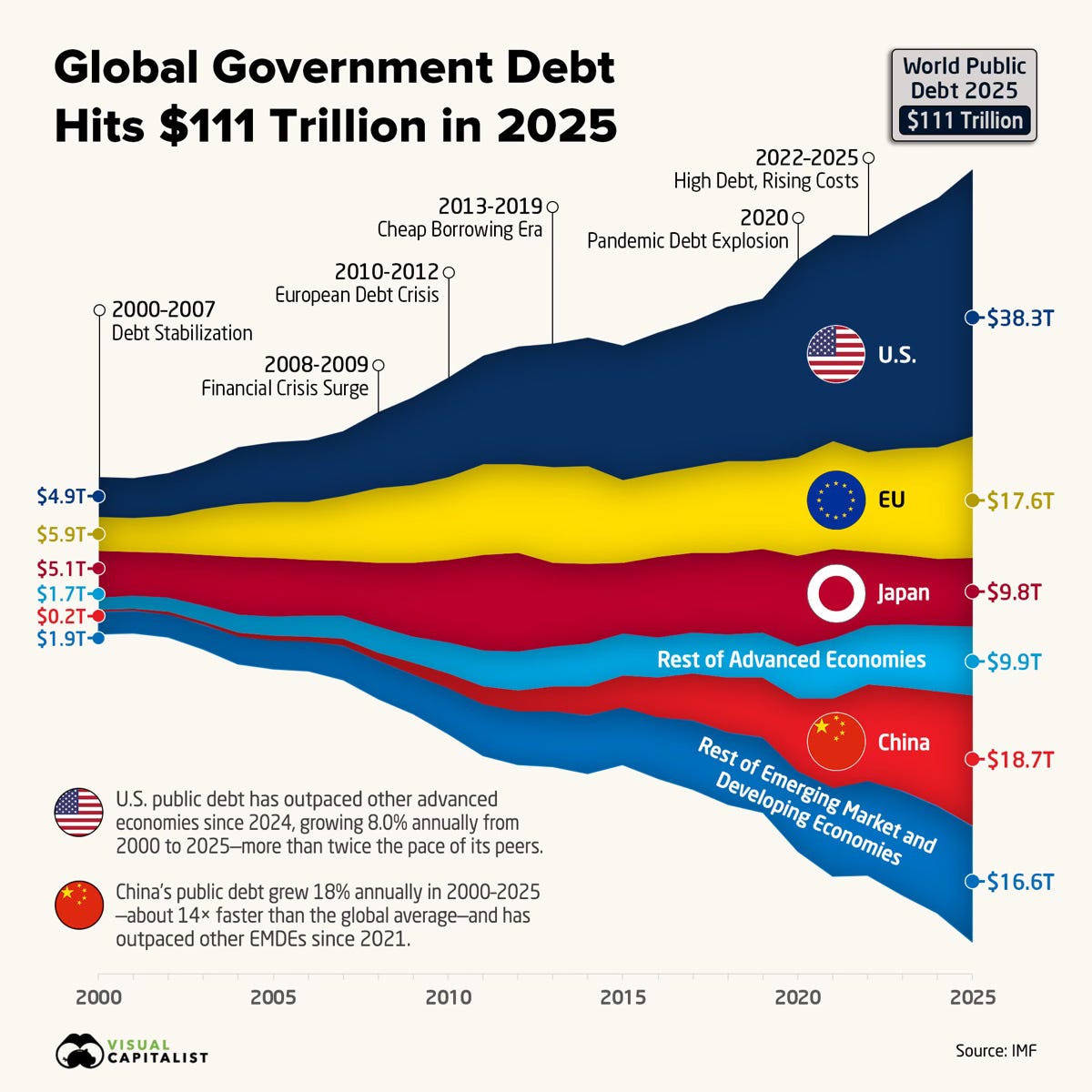

For $10 a month, or $100 a year, you support a simple mission: spread great data visualisation wherever it comes from. You help fund the work of finding, sourcing and explaining the charts that deserve a wider audience. And you back a publication built on generosity, transparency and the belief that better understanding makes a better world.CHART 1 • Why global debt keeps rising even after the crises end

The climb to $111 trillion in global government debt was once easy to explain. The financial crisis pushed borrowing higher, and the pandemic drove it sharply higher again. What is harder to explain is why it has continued to rise after both shocks have passed.

The chart shows that this is no longer crisis driven borrowing. It is structural. The US and China now dominate the picture, accounting for a large share of the increase. In the US, persistent deficits reflect spending choices that have not adjusted to higher interest rates. In China, debt has risen alongside efforts to sustain growth through investment.

What has changed is not just the level, but the nature of borrowing. During the pandemic, debt was temporary by design. Today it is becoming permanent. Governments are issuing at scale without a clear path back.

That matters because the cost is rising. Higher rates turn debt into a constraint rather than a tool. The chart shows accumulation, but the real shift is that the system is no longer correcting itself.

Source: Visual Capitalist

What makes this moment difficult to read is how normal it all appears. Debt rises, markets function, capital reallocates. Nothing feels urgent, and that is precisely the point. The system absorbs more strain without forcing a correction, which makes the underlying shift harder to see.

There is a quiet risk in that. When limits are redefined slowly, they stop feeling like limits at all. Until they are.

I have four more charts that explore where this pressure could surface next and how markets might respond, but they are for paid subscribers. Consider joining if you want the full edition.

{kind=link}