The difficulty with capping credit card rates

Five charts to start your day

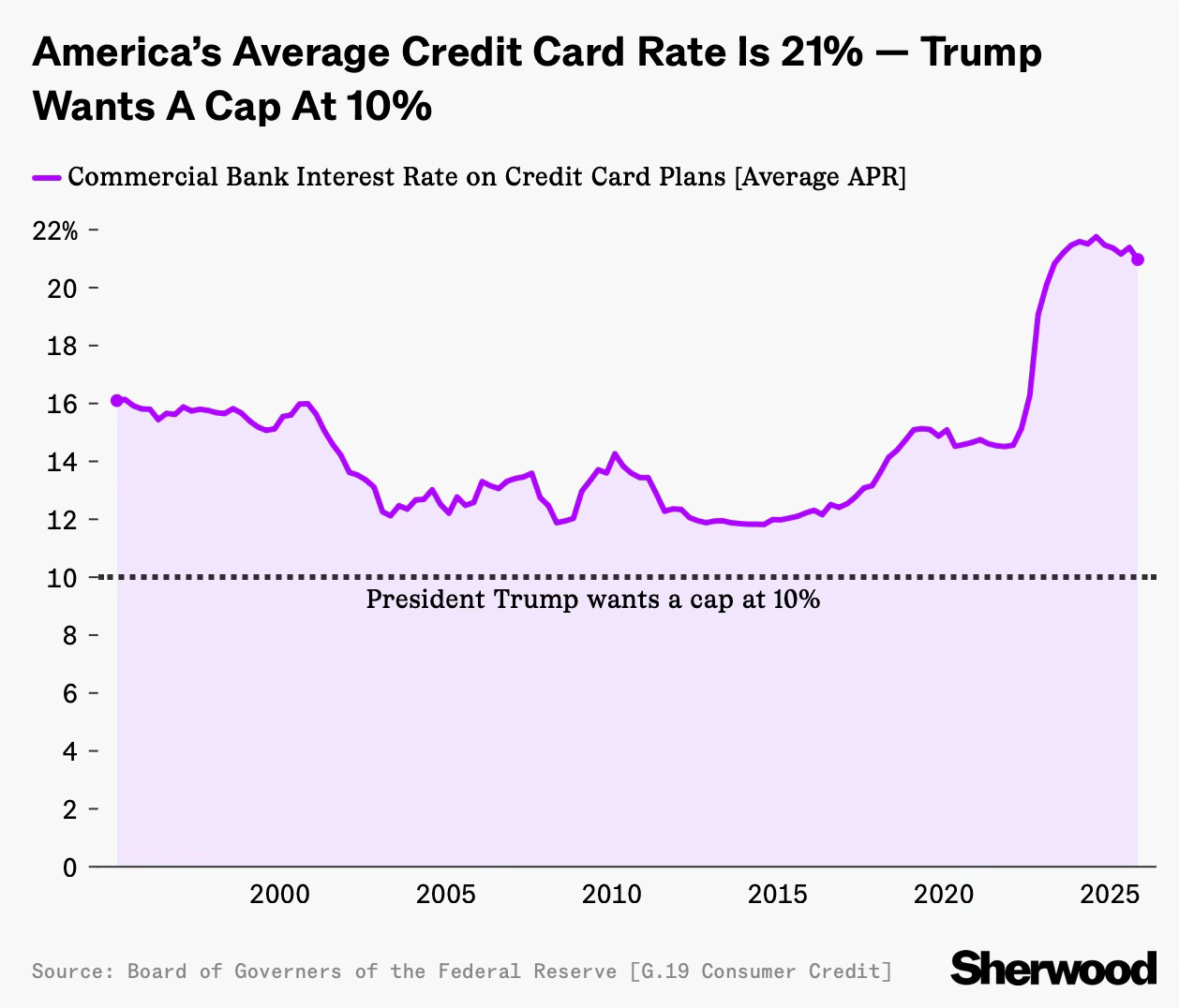

For $10 a month, or $100 a year, you support a simple mission: spread great data visualisation wherever it comes from. You help fund the work of finding, sourcing and explaining the charts that deserve a wider audience. And you back a publication built on generosity, transparency and the belief that better understanding makes a better world.CHART 1 • The difficulty with capping credit card rates

If you have credit card debt in the US, a higher interest rate means more of your monthly payment goes to interest and less goes towards paying the debt down.

The average credit card rate is about 21%. For much of the 2000s and 2010s, it was in the low to mid teens. When the Federal Reserve raised interest rates, credit card rates rose quickly. When other borrowing costs later fell, credit card rates stayed high. A cap at 10% would mean cutting today’s rates by roughly half.

That gap explains why markets reacted when Donald Trump said he wanted to cap credit card interest rates at 10%. As the Financial Times reported, such a cap would require an act of Congress and is unlikely to happen. Even so, shares in large card issuers fell, because their profits depend heavily on current pricing.

It is wrong to think high credit card rates simply follow central bank rates. Credit cards are priced to cover defaults, rewards, fees and profit margins. These costs do not fall just because policy rates fall. A hard cap would force lenders to change products and reduce who they lend to.

If rates were capped this far below current levels, the real issue would not be cheaper credit, but who would still be able to get it.

Source: Sherwood

The credit card chart captures the pattern running through this edition. Nothing has broken. Credit is still available. But at current interest rates, it behaves differently. Carrying a balance is harder to escape, and fewer households can use credit as a short term buffer.

I have four more charts that extend this story and look at where these pressures may surface next. They are for paid subscribers. Consider joining if you want the full edition.