That old lie: bonds returns are negatively correlated to equities

Five charts to start your day

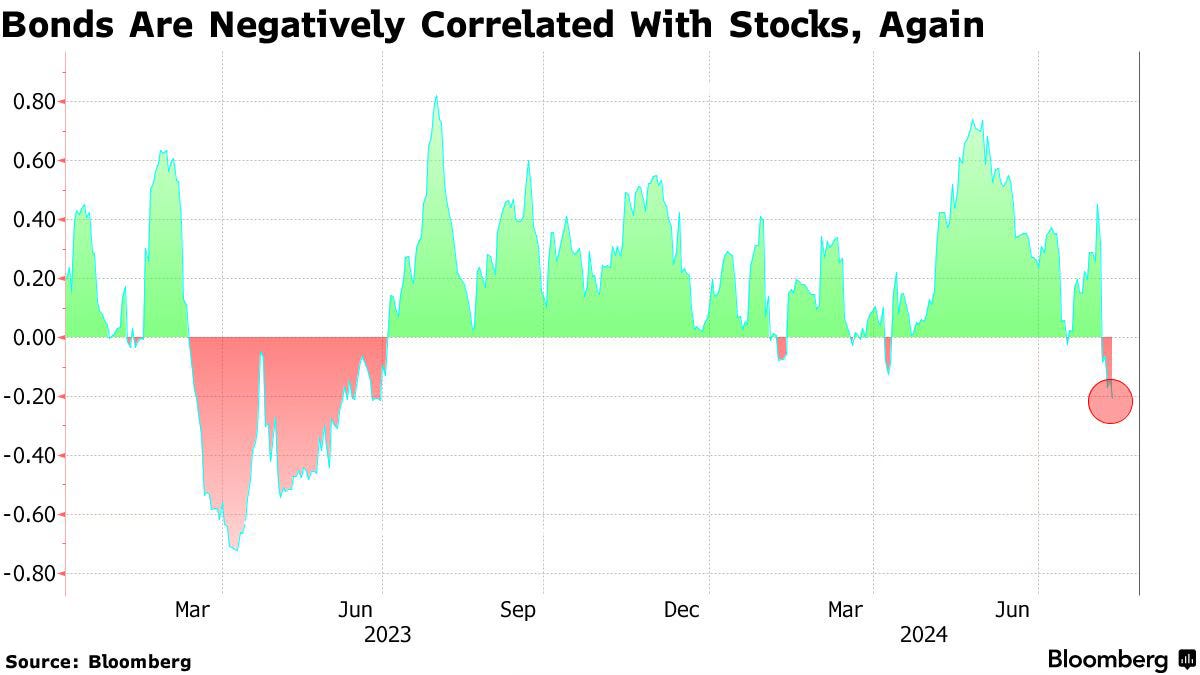

Bonds and equities are negatively correlated, right? Well, yes, then no, then yes again. Look at this chart.

The conventional wisdom is that the returns on equities and bonds are negatively correlated, so there are diversification benefits from combining them.

Source: Bloomberg

There are a few issues with this simplistic view:

"Bonds" aren't a single asset class. For instance, high-yield bonds are more exposed to default risk than long-dated investment-grade bonds, which are more vulnerable to inflation risk.

Therefore, depending on the differing levels of concentration of different types of bond risks within fixed income affects whether “bonds” are positively or negatively correlated with equities at any one point in time.

The S&P 500 is also not perfect. It can rally even when interest rates rise, which is what we have seen in recent years for a variety of reasons.

But there's more bothering me about this Bloomberg chart:

Ridiculously short time period

No defined methodology

Unlabeled y-axis (should be correlation coefficient)

Voters trust Harris significantly more with the economy than Biden

I'm increasingly frustrated with Bloomberg. They're the financial data mafia, and this lack of clarity is annoying. Portfolio managers who manage billions deserve better than just "source: Bloomberg".

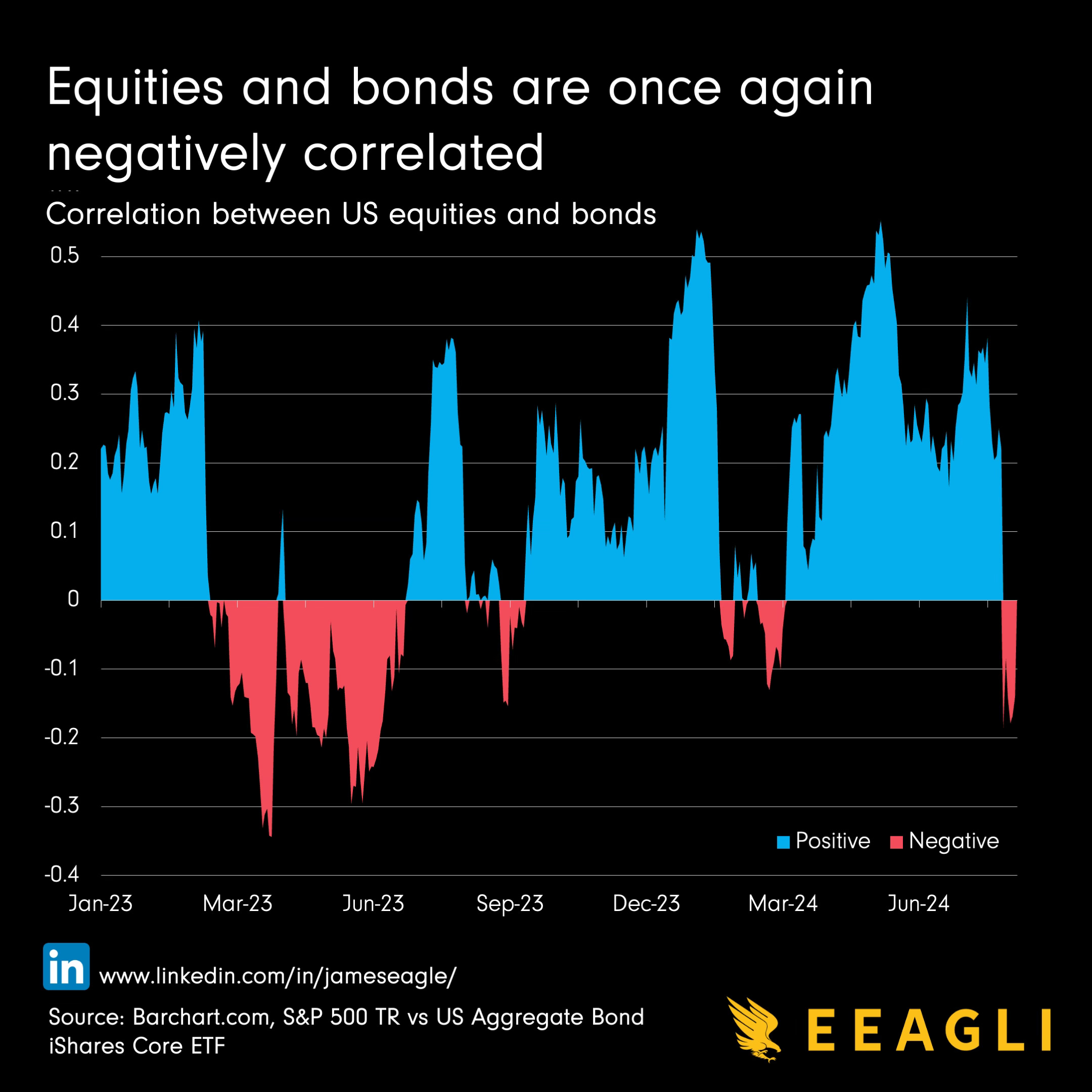

I figured out they used a 21-day rolling period for a US equity index and their own US aggregate bond index. I replicated it using S&P 500 total return and US Aggregate Bond iShares Core ETF. The methodology checks out, but it's hardly a seismic event in asset allocation.

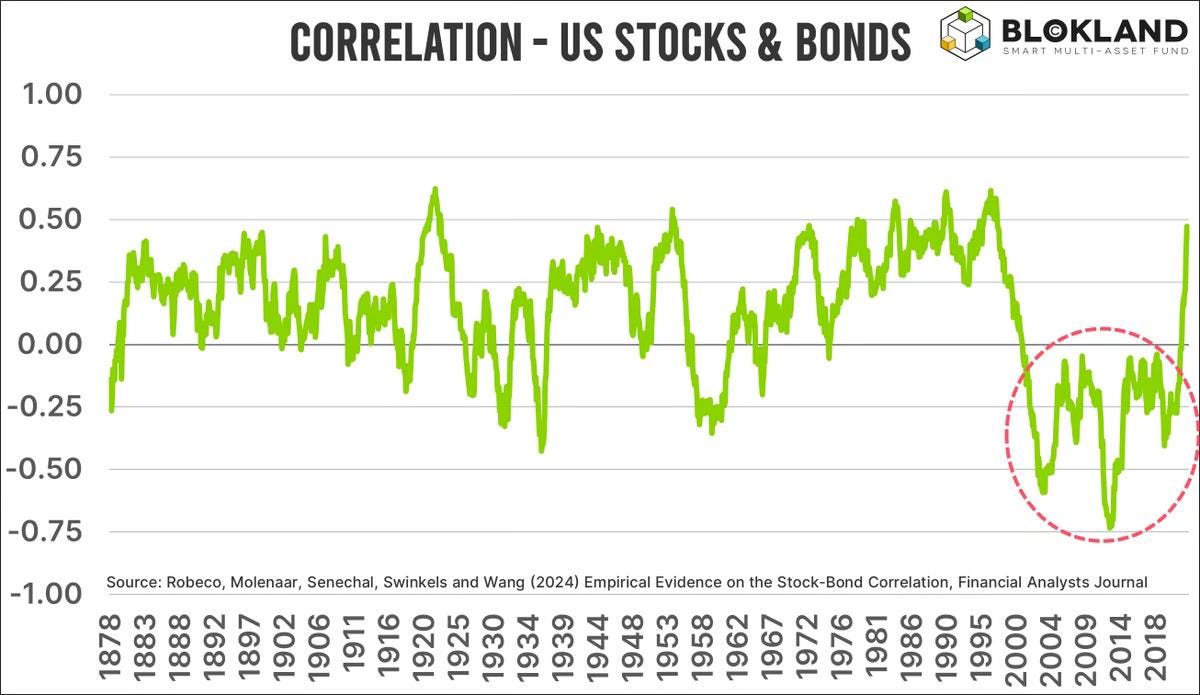

A follower with more asset allocation experience than me, Joeren Blokland (follow him on Substack), wisely told me to "zoom out". This is what he said:

"Most investor generations are (literally) brought up with the idea that the equity-bond correlation must be negative. But this is entirely flawed. For most of history, the correlation has been positive."

He gave me this chart. It’s pretty revealing. That’s 50 years of data and the findings are quite extraordinary. Basically, conventional wisdom on bonds and equities are more wrong than right i.e. US stocks and bonds are positively correlated more often than they are negatively correlated.

Source: Joeren Blokland

Here’s another interesting observation. Recent changes in monetary policy, from rate hikes to potential cuts, has altered the behaviour of bonds.

One of my followers Mike Agne pointed out that this shift could make bonds a more attractive short-term compared to equities, thanks to their price sensitivity to rate changes due to convexity.

Without digging into this very good point, which is a separate topic, this just highlights the complex nature of markets. The environment is constantly changing and it is difficult to predict.

So what can we draw from this. The relationship between bonds and equities is far more complex than often portrayed. As investors, we need to:

Look beyond short-term fluctuations and consider long-term historical trends. (Thanks Jeoren Blokland)

Understand the specific risks associated with different types of bonds and equities.

Rethink our approach to diversification, considering a broader range of factors beyond simple asset class definitions. (Risk-premium investing)

Stay alert to changing market dynamics and their impact on asset correlations (Thanks Mike Agne).

By embracing this complexity, we can build more robust, truly diversified portfolios that are better equipped to navigate the ever-changing financial landscape.

Coming up:

Thousands of millionaires are projected to leave the UK in 2024

Tax Revenue vs. GDP for Major Countries

What election issues are Americans searching on Google?

If you like the sound of that line up, this is usually a paid newsletter. You basically get all my best ideas daily. Hit the subscribe button if you are interested and this will be sent to your inbox daily.