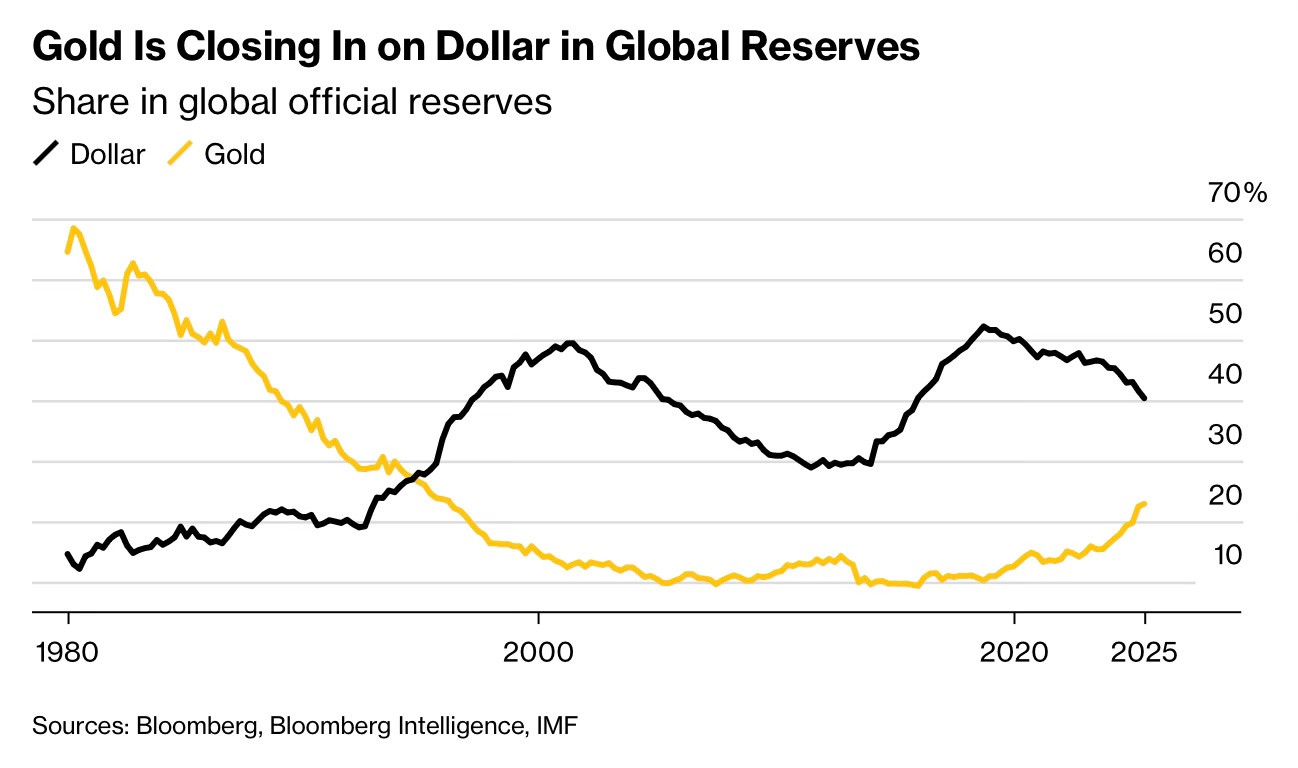

Gold gains on the dollar in global reserves

Five charts to start your day

The dollar is still King. I do not buy the grand de-dollarisation story. What has changed is policy risk under the current tariff regime, and that matters for reserve behaviour. The threat of sweeping new US tariffs, including talk of 100% rates on Chinese goods, has turned trade into an active policy lever again. Beijing is squarely in the line of fire, and escalation is a live risk. In that context it is rational for central banks to trim concentration risk at the margin.

The flows fit this picture. Central banks have been persistent net buyers of gold for three years at historically high levels, while the dollar’s share of disclosed reserves remains dominant but has drifted lower over the long run. Markets frame this as part of the debasement trade, which tends to accelerate when trade tensions flare and US fiscal worries are front of mind. On tariff-heavy days, gold usually moves first.

My view is simple. This is not a revolt against the dollar. It is insurance against tariff-driven shocks and policy unpredictability. Reserve managers are nudging the mix rather than flipping it, adding neutral collateral and shaving a little dollar duration while the United States runs large deficits and trade policy becomes more interventionist. Slow, cumulative diversification is exactly what one would expect in this climate, and the chart shows that shift.

CHART 1 • Gold gains on the dollar in global reserves

The reserve system is shifting. Investors are leaning into what Bloomberg calls the debasement trade as they look to protect savings from the erosion of money. The move is not about deficits alone. It is a broader hedge against policy and geopolitical risk.

The dollar’s share of global official reserves has slipped from around 70% at the turn of the century to about 40% today. Over the same period gold has climbed from single digits to roughly 20% and is still rising. Central banks are diversifying for several reasons. Big fiscal deficits and rising debt loads. Periods of negative or thin real yields. Geopolitical fragmentation and sanctions risk. A desire for neutral collateral that carries no counterparty risk. And a long term push by some countries to reduce reliance on any single currency.

If this mix persists, gold’s role in reserves could keep growing as the dollar’s edge narrows.

Source: Bloomberg