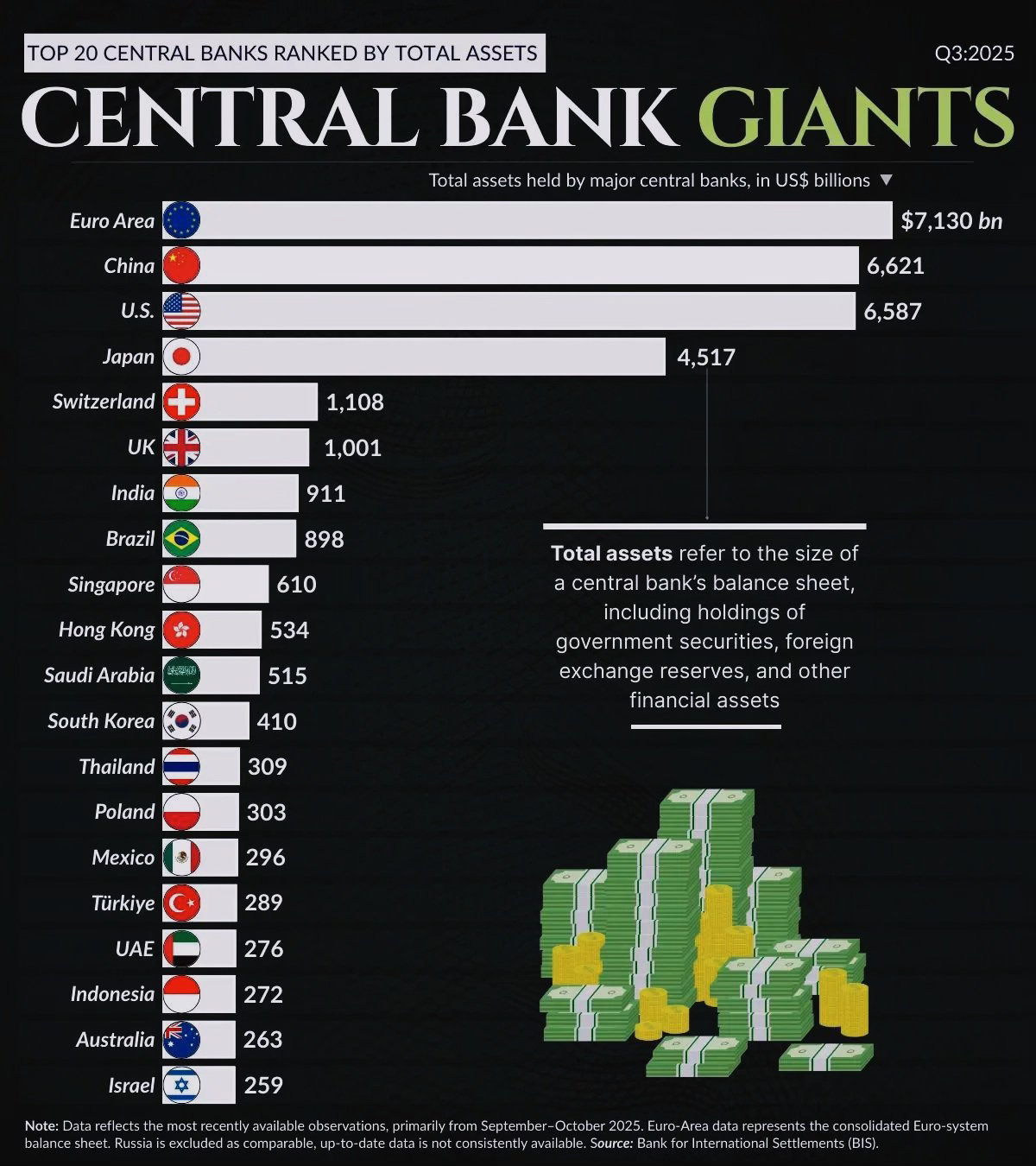

Central bank balance sheets are no longer temporary

Five charts to start your day

For $10 a month, or $100 a year, you support a simple mission: spread great data visualisation wherever it comes from. You help fund the work of finding, sourcing and explaining the charts that deserve a wider audience. And you back a publication built on generosity, transparency and the belief that better understanding makes a better world.

Some things start as emergency measures. We tell ourselves they are temporary, even as the evidence piles up.

These five charts are about permanence. Central bank balance sheets that no longer shrink. Commodity supplies that look ample until you examine how fragile they really are. Resources that exist on paper but not in production. Beneath all of them sits the same tension between theory and reality.

CHART 1 • Central bank balance sheets are no longer temporary

Central banks were once meant to be quiet backstops. This chart shows how far they have moved from that role.

The balance sheets of the Federal Reserve, ECB, Bank of Japan and People’s Bank of China expanded sharply after the financial crisis, surged again during the pandemic and have barely retreated since. Trillions in assets are now held permanently rather than as emergency tools.

This matters because size changes behaviour. When central banks hold large portions of government bond markets, their actions influence yields, liquidity and risk appetite even when policy rates are unchanged. Balance sheets become an active policy channel rather than a background detail.

Attempts at shrinking them have proven slow and politically sensitive. Markets react quickly, governments rely on stable funding and financial systems have adapted to this support.

Central banks still talk like temporary actors. Their balance sheets suggest something closer to permanent institutions of market structure.

Source: Global Statistics

What stands out to me is how often we confuse availability with accessibility. Assets can exist without being usable. Support can exist without being reversible. Once systems adapt to these conditions, stepping back becomes far harder than stepping in.

There is a quiet psychological comfort in believing flexibility always exists. That policy tools can be withdrawn. That supply will respond. That markets will adjust smoothly. History suggests otherwise. Stability often relies on structures we stop questioning once they feel familiar.

I have four more charts that push this theme further and explore where these hidden constraints may surface next. They are for paid subscribers. Consider joining if you want the full edition.