Big Tech is becoming capital heavy

Five charts to start your day

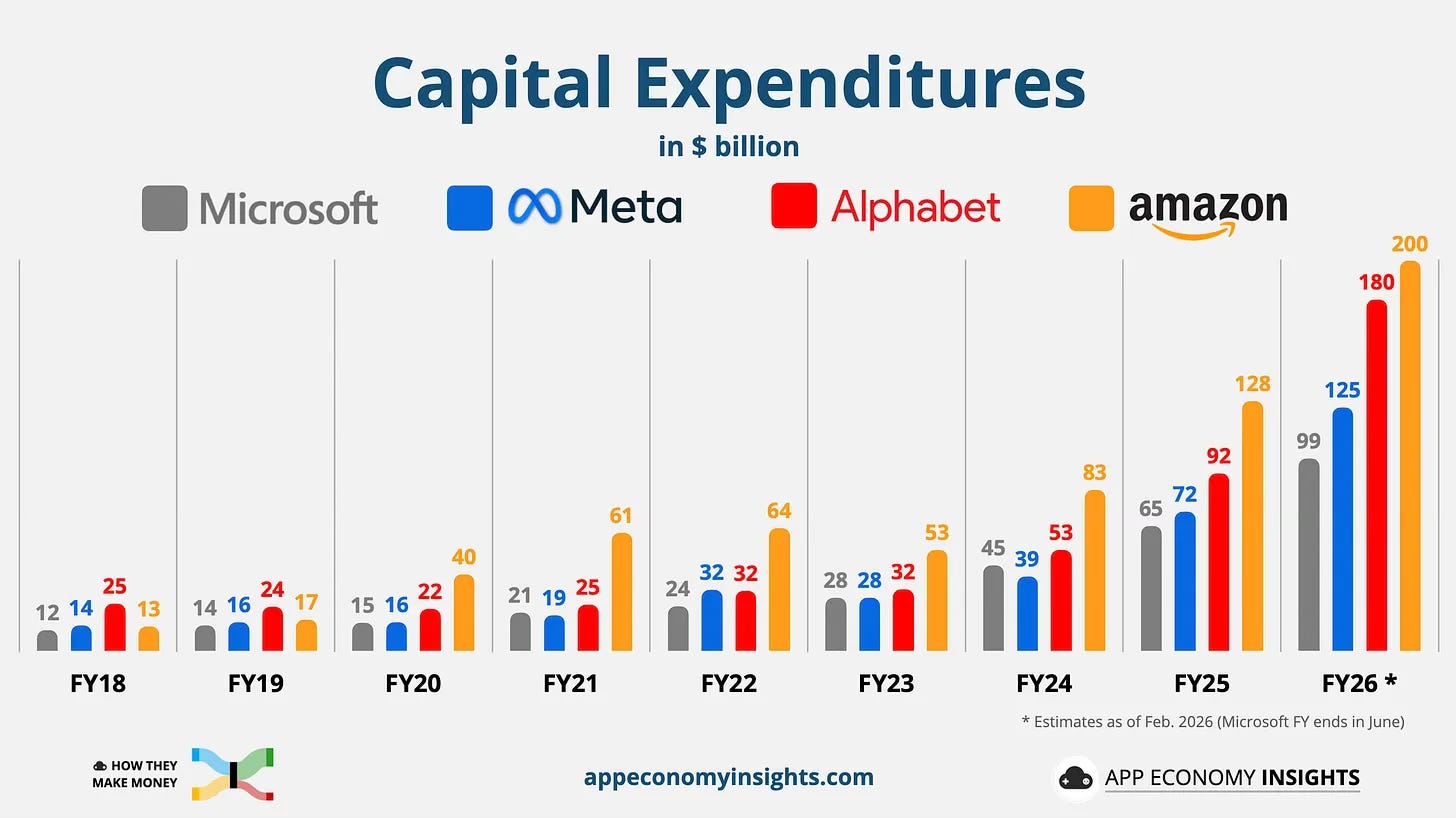

For $10 a month, or $100 a year, you support a simple mission: spread great data visualisation wherever it comes from. You help fund the work of finding, sourcing and explaining the charts that deserve a wider audience. And you back a publication built on generosity, transparency and the belief that better understanding makes a better world.CHART 1 • Big Tech is becoming capital heavy

Something structural has shifted in the business model of the world’s largest technology companies. This chart shows annual capital expenditure at Microsoft, Meta, Alphabet and Amazon rising from roughly $12bn to $25bn in 2018 to between $99bn and $200bn by 2026 on current estimates.

Amazon sits at the top. Its spending rises from $13bn in 2018 to an estimated $200bn by 2026. Alphabet climbs from $25bn to around $180bn. Meta increases from $14bn to roughly $125bn. Microsoft moves from $12bn to just under $100bn. The steepest acceleration comes after 2021, when AI infrastructure spending begins to dominate investment plans.

These figures are broadly consistent with company filings and recent guidance. Amazon and Alphabet have both indicated capital expenditure plans approaching $180bn to $200bn annualised. Meta’s sharp rise reflects its pivot toward AI infrastructure after a period of cost cutting. Microsoft’s financial year ends in June, which affects timing comparisons, but not the direction of travel.

The deeper shift is philosophical. For two decades, large technology platforms were seen as asset light. Software scaled without factories. Margins expanded with limited incremental capital. The AI cycle changes that equation. Data centres, specialised chips, cooling systems and long term energy contracts anchor these companies to physical infrastructure in a way that resembles utilities or telecom operators more than traditional software firms.

Source: App Economy Insights

What strikes me most is not just the scale of the spending, but the concentration of power behind it. A handful of companies are now deploying capital at a level that rivals the annual output of mid-sized economies. Competition begins to look different when the frontier is financed by balance sheets, not just ideas.

I have four more charts that expand on this story and dig deeper into where the risks and opportunities may lie. They are for paid subscribers. Consider joining if you want the full edition and a clearer view of how this capital cycle might unfold.

{kind=link}